For thousands of Kiwis, buying a second property and renting it out is a favourite form of investment. Kiwibank mobile mortgage manager Shane Hawtin knows this – he’s one of them.

“New Zealanders have a real passion for property, and it's been seen as a way of building your capital over time. Depending on the property, it can sometimes be less risky than other investments.”

Investing in a rental property might be an option for a number of people who might not realise it’s an option for them, he says.

As with any major purchase, it’s important to do your homework first, and this certainly applies if you’re considering getting into the rental property market.

Start your property search

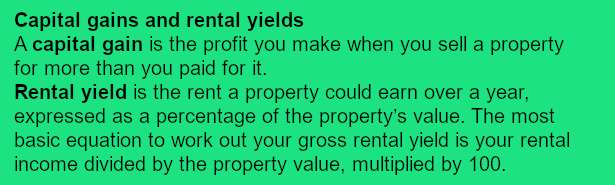

Most investors enter the property market with a focus on either capital gains or rental yield (see below).

For an idea of how different areas stack up, take a look at the QV website, where you can search median rents, annual rent changes, and gross rental yields for different suburbs around the country.

Once you’ve done the prep work, you’ll probably be keen to hit the open home circuit.

When you’re looking for an investment property you need to think with your head, not your heart. Consider things like:

· Location – is it close to public transport, schools, cafes, restaurants and shops?

· Condition – has it been well maintained or will you need to do a lot of work to it? Does it meet the Government’s Healthy Home standards for heating, insulation and ventilation?

· Rent potential – how much rent is it likely to get? Has it been a rental before? If so, can you see how much it rented for and what the occupancy rate was like?

Hawtin advises making contact with the appropriate professionals at each step of the process.

“I would recommend to anybody who's thinking about getting into an investment to make initial contact with the bank to see if it is possible and what it might look like. Then talk to an accountant about the rules around investment. You'll also need to talk to a lawyer as well if you find a property you want to move forward with. So it’s vital to do your research.

“That leads on to some of the risks. Ideally, you want to be aware of any major works that need to be done on the property and to plan for these costs. For example, if major works are required, you should think about budgeting for vacant tenancies and the work itself. It’s important to keep your insurer in the loop so you understand what is and is not covered by your current insurance policy.

“You have to be prepared for movement in house prices and values - just look at the last 18 months, for example, where prices have dropped. And, of course, we’ve seen interest rates significantly moving around over the last 12 to 18 months.”

He says it’s important for potential landlords to decide whether they’ll manage their own property or hand the property over to a rental manager. While the DIY approach may save on fees, it also means dealing with tenants, possibly late rental payments and Tenancy Tribunal disputes, and organising maintenance contractors.

If that sounds a bit off-putting, Hawtin has some words of encouragement from his personal experience. “I've been working at Kiwibank for 16 years so there's not much I haven't seen when it comes to the property market. In addition to that, I've been able to invest in rental properties myself so I come from a place of really understanding how to go about it.”

Naturally, when talking about a sizeable investment such as a property, and when a number of professionals such as lawyers, bankers, accountants and insurance companies are likely to be involved in the process, quite a number of technical terms come up in conversation. Hawtin is aware that these are likely to confuse or surprise the would-be investor, so he and the Kiwibank experts have attempted to explain them in everyday language.

‘Unlocking equity’

Simply put, “unlocking equity” is using the value that you have in your existing assets to secure lending without actually needing a cash deposit for the asset you are wanting to purchase. How you work out your equity is to take the total value of your properties minus any debts. For example, if the market value of your home is $500,000 and the balance of your home loan is $200,000, then your equity would be $300,000. Where your existing equity may not be enough, you can also add cash to make up the deposit requirements.

Loan-to-value ratio

The Reserve Bank has determined that in most scenarios, the maximum amount you can borrow to purchase an investment property is 65% of the value of that property. To put it another way, you need 35% cash or equity available for every $100,000 you spend on the property. For example, if you’re purchasing for $500,000, you need $175,000 cash or equity available that you can borrow against. All banks need to adhere to this requirement. You can’t use all of the equity from your owner-occupied house – your bank will usually want you to leave at least 20% of the value of your property as equity in that house. The bank will also take other things into consideration like your income and the potential rental income of the investment property.

Bright-line test

If you sell residential property before owning it for ten years (or five years if it’s a new build), you may need to pay income tax on any profit you make on the sale. This is called the bright-line test. There are rules around who is and isn’t captured by the bright-line test so, it’s important to check with an accountant to confirm what tax rules might apply to you.

Tax deductions

Currently tax deductibility is generally only available for new builds. It is not available for second-hand (or previously lived in) properties purchased as investments. However, an accountant will be in the best position to advise you on your individual circumstances. The new government has discussed making some changes to the rules – see below.

Change of government

There is discussion around the new Government making changes to these rules. It’s being proposed that the bright-line test would be reduced to two years only and there will be a change to tax deductibility rules. The new government has pledged to reverse the Labour government’s decision to abolish landlords’ ability to deduct their interest costs from their overall tax bill. The new government’s decision will effectively reduce the tax bills of individuals who own multiple residential properties. It's anticipated that this change will take place in the current tax year.

Interested in an investment property?

You may be able to join the property investor ranks by tapping into the equity of your current home or becoming a "rentvestor" if you're a first-time buyer.

For more information, see kiwibank.co.nz/personal-banking/home-loans/getting-a-home-loan/investing-property/